One Stop Europe

- Home ›

- One Stop Europe

A Single Digital E-Commerce Market

On 1 July 2021, the rules and regulations for importing goods into the EU changed fundamentally, creating a single e-commerce market and digitalizing the operating environment for logistics and commerce stakeholders along the entire delivery chain

, and flourish in the single e commerce market.")

At A Glance

- 1 July 2021: EU eCommerce VAT Package – the mandatory digital handling of import customs & VAT

- 1 January 2021: UPU – mandatory electronic advanced notification (EAD) for cross-border commercial items

- Changes create new options for reducing cost, boosting quality and increasing control and flexibility along the entire delivery chain.

The European Union

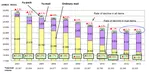

(EU) is a major e-commerce market, with the number of e-commerce users expected to hit 564 million by 2025.

B2C e-commerce revenue in Europe is projected to exceed EUR 750 billion in 2022, growing (CAGR 2022-2025) at 13.83% a year to reach a market volume of EUR 1,100 billion by 2025. [1]

Around a 1/4 of all consumer purchases are made from sellers based outside Europe.[2]

2021 heralded a truly digital e-commerce market

The EU eCommerce VAT package[3], which came into effect on 1 July 2021, revolutionizes Europe's e-commerce market.

The digital handling of import customs and VAT on all transactions became mandatory, with import VAT due on each and every shipment sent to the EU.

This is a disruptive change, and will gradually lead to the emergence of a whole range of new business models.

It brings to an end to the current dominance enjoyed by EU postal operators in importing ecommerce shipments, together with their monopoly on paper-based customs clearance.

This development is further accelerated by

fundamental changes in postal pricing, such as dramatic increases in UPU rates.

Furthermore, shipping, customs

clearance and import VAT management are all becoming separate transactional

workflows. This creates new options for e-commerce marketplaces and online merchants,

and offers greater flexibility for optimizing commerce logistics and

last-mile-shipping within the EU.

And as if all that weren’t enough, new EU standards are also emerging, involving more local obligations to digitally register and notify authorities (e.g. waste management).

How the EU ecommerce VAT Package fundamentally changed the e-commerce market from 1 July 2021:

- Abolition of the import VAT threshold limit (de minimis rule) for low value B2C consignments below 22 EUR – VAT is payable on all goods imported into the EU.

- Import-One-Stop-Shop model (IOSS) to manage all local import VAT (all EU target countries consolidated under a single tax identification number and account and registered with one selected EU tax authority).

- Shipments valued under €150 are exempt from import VAT when the Import-One-Stop-Shop is used, with digital customs (pre-)declaration enabling digital clearing and seamless border-crossing where import VAT payment liability is clearly documented.

- Marketplaces (“deemed suppliers”) liable for the payment of import VAT.

- Removal of de-facto customs clearance privilege enjoyed by designated postal operators with the end of paper-based customs clearance for low-value consignments (below €22) = over 2/3rds of cross-border shipments to the EU ecommerce market.

- Customs, import VAT and shipping channels become independent entities – opportunity for importers to optimize flexibility and cost by choosing different service providers for each transactional channel.

New operating environment throws up extensive challenges…..

On 1 January 2021, the Universal Postal Union (UPU) introduced mandatory electronic advanced data (EAD) notification for every individual cross-border commercial mail item destined for delivery within the networks of designated postal operators worldwide.

In addition, current developments at UPU level, in particular rising UPU tariffs, make the previous, often preferred model of the “classic postal channel”— sender hands mail to a non-EU postal operator which forwards it to an EU postal operator for customs clearance and delivery — increasingly unattractive.

Users of this traditional channel now need to look for new and efficient customs clearance and VAT solutions.

These solutions are independent

of the mail item delivery itself so that, following customs clearance, the

sender is free to choose the optimal delivery channel for these items within

the EU (e.g. remain within UPU channel, direct entry to the postal channel in the

EU, commercial delivery solutions).

….as well as opportunities

These omnichannel and

multicarrier solutions may increase complexity and the demand for local know-how, but they

also provide interesting options for reducing cost, boosting quality and

increasing control and flexibility along the delivery chain, starting well

before the collection of postal items and ending well after last mile delivery.

All of this will have a significant impact on cross-border commerce and imports into the EU.

Global impact on logistics & commerce

The greatest impact in the e-commerce market will be felt by shippers importing consignments of goods into the EU – not only those based in the major Asian marketplaces, and eShops, but also shippers in markets such as Switzerland, USA, Canada and Russia.

Logistics service providers outside the EU, both designated postal operators and commercial companies, face the same set of challenges.

They will need to implement digitalized cross-border logistics solutions for imports into the EU, provide their customers with relevant and flexible digital solutions, and comply with the new rules and regulations – all whilst retaining their competitive edge.

No stone left unturned

The COVID-19 pandemic has only accelerated this development.

Already, there are clear indicators that when cross-border transport

capabilities are reestablished, buyers will revert from their current local

focus to options in which the primary consideration is cost.

Where e-commerce market stakeholders successfully adapt to

the new environment and create the digital capabilities required to exploit these

new business opportunities, growth rates for inbound volumes to the EU will grow at a

scale hitherto unknown.

For more about this subject, check out the articles in the E-Commerce Market series below, and come back regularly for updates.

Need more information, insights, or support? Contact the Commerce Logistics Specialists directly.

[1] https://www.statista.com/outlook/dmo/ecommerce/europe [2] Europe 2020 Ecommerce Region Report, published by Ecommerce Europe & EuroCommerce [3] On 5 December 2017 the Council adopted the VAT e commerce package consisting of: Council Directive (EU) 2017/2455, Council Regulation (EU) 2017/2454, and Council Implementing Regulation (EU) 2017/2459

Does this article cover a topic relevant to your business? Access the CLS Business Lounge for the market intelligence you need to stay ahead of the crowd. Find out more

READY TO UPGRADE?

Secure your seat in the CLS Business Lounge – premium market intelligence & insights + one-on-one business support each month.

Recent Articles

-

The PPZ: A Blueprint for Postal Cross-Border Ecommerce & Logistics

Mar 10, 26 09:30 AM

Discover the Postal Prosperity Zone (PPZ), a tried and tested blueprint for efficient and effective postal cross-border ecommerce and logistics.

Discover the Postal Prosperity Zone (PPZ), a tried and tested blueprint for efficient and effective postal cross-border ecommerce and logistics. -

The Postal Prosperity Zone: How Posts Lost Control and Volume

Mar 10, 26 07:01 AM

Designated Operators currently play only a minor role in cross-border ecommerce—they can regain leverage, data, and margins with the Postal Prosperity Zone.

Designated Operators currently play only a minor role in cross-border ecommerce—they can regain leverage, data, and margins with the Postal Prosperity Zone. -

The evolution of postal tariffs: past, present & future

May 25, 23 04:16 AM

Postal tariffs from the 1970s to the present: how terminal dues and changing rate systems reflect international development and shape the global postal network.

Postal tariffs from the 1970s to the present: how terminal dues and changing rate systems reflect international development and shape the global postal network.

Cross-Border Ecommerce: Creating the Digital Single Market

Walter Trezek in Logistik Express on cross-border ecommerce, and industry association Ecommerce Europe creating standards for the digital single market

Japan Post: Responding To Ecommerce Growth & Shrinking Mail Volumes

Best practice series: Japan Post has stabilized failing mail volumes and introduced new products and services to support ecommerce growth.

The PPZ: A Blueprint for Postal Cross-Border Ecommerce & Logistics

Discover the Postal Prosperity Zone (PPZ), a tried and tested blueprint for efficient and effective postal cross-border ecommerce and logistics.

Postal customs clearance procedures and the EU VAT Ecommerce Package

Exploring changes to postal customs clearance procedures and VAT payments following the 1.7.2021 EU VAT Ecommerce Package.

READY TO UPGRADE?

CLS Business Lounge: Get the market intelligence & insights you need to thrive in a disruptive business environment.